Top Glove Corporation Bhd

(Company No. 199801018294 [474423-X])

Top Glove Media Contact:

Michelle Voon

[email protected]

+603-3362 3098 Ext 2228

+6016 668 8336

Investor Contact:

Qiuvy Chong

[email protected]

+603-3362 3098 Ext 2234

+6012 265 8973

PRESS RELEASE

For Immediate ReleaseTOP GLOVE CONTINUE TO MAKE PROGRESS IN THE FOURTH QUARTER DESPITE CHALLENGES

Financial results for the fourth quarter and full year ended August 31, 2011

Klang, Tuesday, October 11, 2011 –Top Glove Corporation Bhd (Top Glove) today announced, its revenue for the fourth quarter ended August 31, 2011 (4QFY11) rose 1.2% to RM541.84 million from RM535.36 million in the preceding quarter, while net profit increased 3.2% to RM26.87 million from RM26.04 million, as the more stable latex prices in this quarter had reduced the impact of time lags in cost pass-through.

For the 12 months, Top Glove’s revenue declined marginally to RM2.05 billion from RM2.08 billion a year ago, while net profit declined 54% to RM115.19 million from RM 250.41 million. The decline in profit was principally due to the continuously high volatility in latex price, the weaker US dollar against the Ringgit Malaysia and the oversupply situation in the industry which resulted in a lower cost pass through to the customers.

For the 12 months, Top Glove’s revenue declined marginally to RM2.05 billion from RM2.08 billion a year ago, while net profit declined 54% to RM115.19 million from RM 250.41 million. The decline in profit was principally due to the continuously high volatility in latex price, the weaker US dollar against the Ringgit Malaysia and the oversupply situation in the industry which resulted in a lower cost pass through to the customers.

Compared with last year, the average natural latex prices rose by 45.8% (from RM6.12/kg in FY2010 to RM8.92/kg in FY2011) while the average US dollar against the Ringgit weakened by 8.1% (from RM3.32 in FY2010 to RM3.05 in FY2011).

The comparability of the figures is also affected by the previous year's exceptionally high earnings, which had been boosted by the surge in demand for rubber gloves during the influenza A(H1N1) virus outbreak.

Top Glove also announced that the Board of Directors has proposed a final single tier dividend of 6 sen per share, subject to shareholder’s approval at the forthcoming AGM.

Top Glove Group Chairman, Tan Sri Lim Wee Chai commented, “Despite the weaker profit, the group's earnings is still positive and our cash position remains strong, enabling the company to pay 11 sen full year dividend, which is equivalent to a 60 % payout ratio”.

The management has taken serious measures to tackle these headwinds and has succeeded in reducing their impact. As before, Top Glove continued to share some of these higher costs with its customers and hedge its open foreign exchange position.

At the same time, the Group is focused on planning for the longer term. In order to mitigate the volatility in latex costs in the future, Top Glove has been working on acquiring land in Cambodia, Malaysia and Indonesia, for rubber plantation development to meet its own latex needs.

“We are still in the process of securing the land, as the land approval process has taken far longer than expected. We will continue to look for land as we need at least 40,000 ha to 50,000 ha of land to supply at least 50% of our latex requirements, including requirements from our new factories in the future,” said Tan Sri Lim.

Simultaneously, Top Glove has been increasing the production of nitrile gloves to avoid over-reliance on natural rubber gloves.

“Our nitrile glove business is doing well and is increasing. Contribution of nitrile glove sales to our total sales volume increased from 7% in Q1 to 14% in Q4. We are targeting for at least 15% to 17% contribution from nitrile gloves by December 2011,” said Tan Sri Lim.

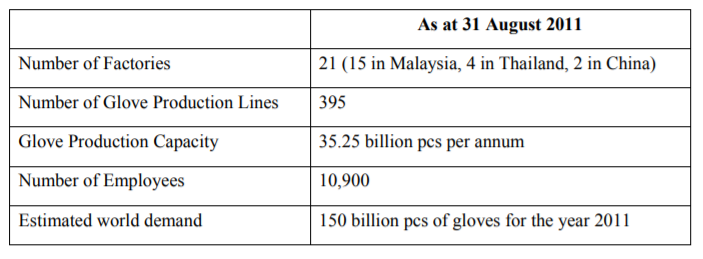

Top Glove’s current capacity expansion projects are mainly to cater to the demand for nitrile gloves. By the end of May 2012, with the factory expansions and the completion of new facilities, the total Group capacity will have increased to around 41.55 billion pieces of gloves per annum.

Top Glove is also investing in more highly automated production lines to ensure more efficient production of consistently high quality products.

As for concerns about the removal of subsidies on gas, Tan Sri Lim commented that Top Glove will continue to diversify its sources of energy to avoid over-reliance on natural gas. Since 2005, it has been investing in biomass facilities to produce the heat energy required by its factories. Going forward, all new factories will also be utilising biomass fuel instead of natural gas.

On the future outlook, Top Glove expects the business landscape to remain challenging with the volatility in the global economic sentiment, commodity prices and foreign exchange, being the major causes for concern.

However, Tan Sri Lim said he is confident the Group will be able to weather the challenges ahead, as they have been through many cycles in the glove industry. “We are keenly aware of today’s industry scenario and remain steadfast in achieving our objectives. We will continue to maintain our emphasis on product quality, protecting market share and gross margins whilst keeping a tight control of the cost base,” said Tan Sri Lim.

Please refer to attached file for additional information on Top Glove’s performance. For more information on Top Glove Corporation Berhad, please visit www.topglove.com.my

About Top Glove Corporation Berhad

Top Glove Corporation Berhad was listed on the Second Board of the Kuala Lumpur Stock Exchange in 2001 and was transferred to the Main Board on 16 May 2002. The company is one of the component stocks of the FTSE Bursa Malaysia (“FBM”) Mid 70 Index, FBM Top 100 Index and FBM Emas Index.

Top Glove is currently the world’s largest rubber glove manufacturer with a good and established corporate culture and business direction of producing consistently high quality, cost efficient gloves. Top Glove has more than 1,000 customers worldwide and exports to more than 180 countries.

Summary of key information:

.jpg)

(1).jpg)

.png)

.png)

.png)

.png)

.png)

.png)