Top Glove Corporation Bhd

(Company No. 199801018294 [474423-X])

Top Glove Media Contact:

Michelle Voon

[email protected]

+603-3362 3098 Ext 2228

+6016 668 8336

Investor Contact:

Qiuvy Chong

[email protected]

+603-3362 3098 Ext 2234

+6012 265 8973

PRESS RELEASE

For Immediate ReleaseHEALTHY GROWTH IN CHALLENGING TIMES

Group posts higher quarter-on-quarter Revenue and Profit amidst cost increases

Shah Alam, Thursday, 16 March 2017 – Top Glove Corporation Bhd (“Top Glove”) today announced its financial results for the Second Quarter ended 28 February 2017 (“2QFY17”), posting improved Sales Revenue amidst an increasingly challenging business environment.

The Group achieved 2QFY17 Sales Revenue of RM851.5 million, an increase of 8% compared with 1QFY17. Profit Before Tax and Profit After Tax were also on the rise, coming in at RM102.7 million and RM83.2 million, respectively representing an increase of 14% and 13% against 1QFY17. Sales Volume (quantity sold) eased 1% quarter-on-quarter, owing to shorter work months during the quarter in review, but was up 9% compared with 2QFY16.

Top Glove’s strong performance despite less favourable conditions, was attributed to improvements adopted across the manufacturing process, which enabled the Group to maintain good quality while managing its costs efficiently. Upward price revisions implemented, the effects of which were felt in 2QFY17, were also instrumental in normalising Sales Revenue figures vis-à-vis the previous quarter.

Year-on-year, Sales Revenue grew by 23%. However, Profit After Tax was softer by 21% versus 2QFY16, on the back of sharp increases in raw material prices, unlike the corresponding period in FY16.

For 1HFY17, Top Glove recorded Sales Revenue of RM1.6 billion demonstrating growth of 10%, while Sales Volume also trended upward by 8% compared with 1HFY16. Meanwhile, Profit After Tax registered at RM156.8 million, easing 33% from 1HFY16, again attributed to higher raw material prices in 1HFY17. Whereas in comparison with 2HFY16, Profit After Tax went up by 22%.

Meanwhile, in 2QFY17, the average latex price surged to a 5-year high, rising 33% to RM5.95/kg compared with 1QFY17 and 72% compared with 2QFY16. The average price for nitrile also increased to USD1.08/kg, going up 10% compared with 1QFY17 and 12% compared with 2QFY16. The sharp rise in raw material prices have steadily driven average selling prices (ASPs) up.

Tan Sri Dr Lim Wee Chai, Top Glove Corporation Bhd’s Executive Chairman remarked: “We have delivered a healthy set of numbers for our 2QFY17, despite a challenging business environment with sharp increases in manufacturing cost. This shows that our approach of focusing on internal factors within our control, such as quality and cost efficiency, and not external factors, is the correct way forward for our business”.

As an essential item in the medical sector, the global demand for gloves is expected to continue growing by 6% to 8% every year. To ensure Top Glove is ready to meet demand both in developed and emerging markets, it is steadily expanding its operations. Construction of a new facility, Factory 30 (Klang) is almost completed and is expected to commence production by May 2017 with a production capacity of 4.4 billion gloves per annum. Meanwhile, additional new facilities in Klang, Factory 31 and Factory 32 will respectively commence operations by November 2017 and December 2018, with a production capacity of 2.8 billion and 4.8 billion gloves per annum. By December 2018, the Group is projected to have 632 production lines and a production capacity of 60 billion gloves per annum. Towards improving operational efficiency and increasing automation, Top Glove has also been working with government agencies and domain experts to develop Industry 4.0 applications, which it is in the process of implementing throughout its factories. As a matter of course, it is concurrently exploring mergers and acquisitions and joint ventures with good valuations in similar or related industries.

As at 28 February 2017, the Group maintained a positive net cash position of RM38.6 million and a healthy balance sheet.

Looking ahead, the Group expects the business environment to be increasingly challenging, with competition intensifying on a larger scale. Given the high raw material price position, the Group will also have to rely on its good relationships with customers to share out the cost increases. However, in line with industry practice, cost savings when raw material prices decrease, will also be passed on customers. Top Glove is of the view that raw materials prices will stabilise at current levels or possibly be on the downtrend, going forward.

Nonetheless, Top Glove remains optimistic on industry outlook given the resilient nature of the industry. Tan Sri Dr Lim asserts, “We have done well in what is considered a softer and challenging quarter. However, we aim to do even better and will continue to strengthen our glove quality, costing and competitiveness in the coming quarters”.

__ ### __

About Top Glove Corporation Bhd

Top Glove Corporation Bhd is listed on the Bursa Malaysia Stock Exchange Main Board and Singapore Exchange Mainboard. It is also one of the component stocks of the FTSE Bursa Malaysia (“FBM”) Mid 70 Index, FBM Top 100 Index, FBM Emas Index, FBM Emas Syariah Index, FTSE Bursa Malaysia Hijrah Shariah Index and FTSE4Good Bursa Malaysia Index. Top Glove is currently the world’s largest rubber glove manufacturer with an established corporate culture and good business direction of producing consistently high quality, cost efficient gloves. Top Glove has over 2,000 customers worldwide and exports to more than 195 countries.

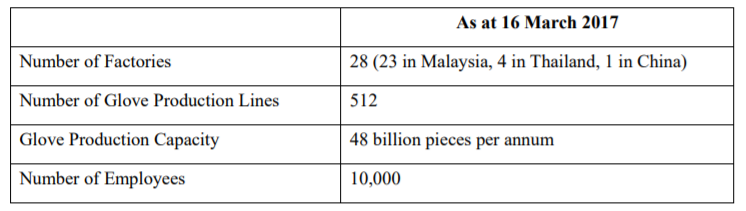

Summary of key information:

.jpg)

(1).jpg)

.png)

.png)

.png)

.png)

.png)

.png)